MUMBAI: Most of the recent market focus has been on the rupee’s modest gains against the dollar. Yet, a closer inspection of currency trends reveals a broader bout of weakness: The Indian currency slid against a basket of non-dollar counterparts, notably the euro and the pound, complicating the picture for policymakers and market participants.

Abhishek Goenka, chief executive of IFA Global, highlighted the rupee’s decoupling from the greenback’s trajectory. “A weaker rupee against non-dollar currencies is positive for exporters, provided they are not overhedged,” he said, noting that the euro and UK pound touched new highs against the rupee.

“It’s a great time for those receiving inward remittances in these currencies,” he added, suggesting risk reversals as a hedging strategy for exporters. He linked the dollar’s softening to a waning geopolitical hegemony: “The central role that the US used to play in global geopolitics allowed it to enjoy exceptionalism. That exceptionalism is now under serious threat.”

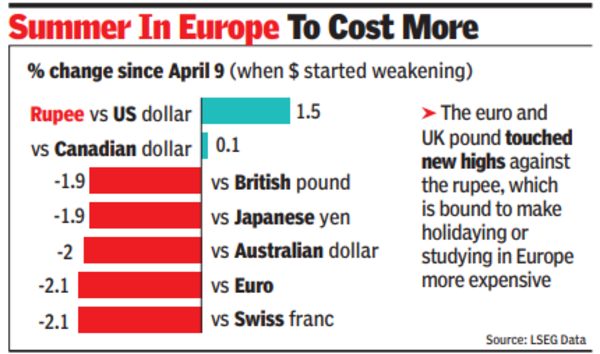

Forex consultant KN Dey saw the dollar’s retreat as a result of the Trump administration’s delay in implementing new tariffs. He pointed to the euro’s ascent to 1.15 – significant, as it constitutes 57% of the dollar index. While this bolstered India’s foreign exchange reserves, he cautioned that “it would also make travel to Europe and education very expensive”. Dey added that European govts, grappling with economic weakness, are unlikely to tolerate prolonged currency appreciation and may act to curb it.

Riya Singh of Emkay Global noted that the dollar index (DXY) fell from 110.17 to below 98, a slide that buoyed non-dollar currencies. “As for de-dollarisation, it appears unlikely in the near term,” she said. “The recent decline in the US dollar seems more driven by policy uncertainties under the Trump-era narrative, economic slowdown concerns, and expectations of 80-100 basis points of rate cuts by the Fed year.” While acknowledging some diversification into gold, Singh argued that “a full-scale shift away from the dollar remains both costly and largely unproven.The dollar still accounts for the majority of global forex reserves, trade settlements, and SWIFT transactions.”

Harsh Madhusudan Gupta of Ionic Asset expects the rupee to gain both in real and nominal terms, though he is sceptical of de-dollarisation. “The trade surpluses that other countries had with the US were being recycled into US treasuries-i.e. they were funding US debt and helping support the US dollar,” he said. “With the imposition of tariffs, the US will still require to import goods as domestic supply would not be able to cater to the demand.It therefore could result in durable inflation in the US, making US real rates more negative. This would cause the dollar to weaken.”